Mortgage Insurance is a financial protection product commonly associated with home loans. It is designed to reduce risk for lenders when borrowers purchase a property with a smaller down payment. Understanding Mortgage Insurance is important for homebuyers because it can affect monthly housing costs, loan qualification requirements, and overall borrowing expenses.

While this coverage may increase the cost of a home loan, it can also make homeownership accessible for borrowers who may not have a large down payment available. The specific requirements and coverage details vary depending on the loan type, lender, and applicable regulations.

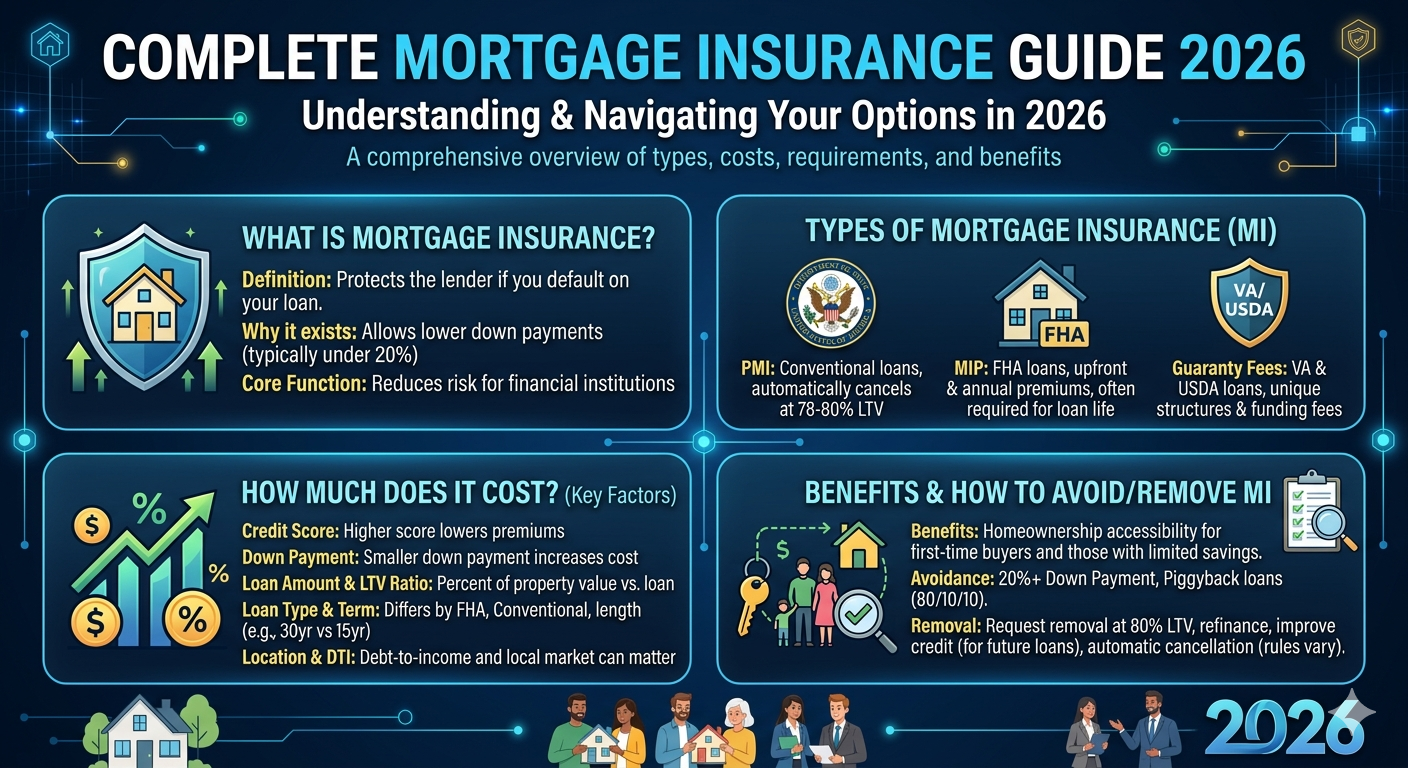

What Is Mortgage Insurance?

Mortgage Insurance is a policy that helps protect the lender against certain financial losses if a borrower is unable to repay a home loan according to the loan agreement.

Unlike homeowners’ insurance, which protects the property owner against covered property losses, Insurance primarily benefits the lender by reducing lending risk.

How Mortgage Insurance Works

When a borrower obtains a mortgage with a lower down payment, the lender may require insurance coverage as a condition of loan approval. The borrower typically pays the insurance premium, while the lender receives the financial protection provided by the policy.

If the borrower defaults on the mortgage and the lender experiences a covered loss, the insurance may reimburse part of that loss according to policy terms.

The presence of this coverage can allow lenders to offer financing options that might otherwise be considered higher risk.

Types of Mortgage Insurance

Government-Backed Loan Insurance

Certain government-supported loan programs may require insurance premiums or guarantee fees that function similarly to mortgage insurance.

Requirements vary according to program guidelines and lending rules.

Lender-Paid Mortgage Insurance

In some cases, lenders may arrange coverage and incorporate the cost into the loan’s overall pricing structure.

Borrowers should carefully evaluate total borrowing costs when comparing options.

Mortgage Protection Insurance

Mortgage protection insurance is different from lender-focused mortgage insurance. It is designed to help borrowers or their families manage mortgage payments under specific covered circumstances.

Who May Need Mortgage Insurance?

- First-time homebuyers

- Borrowers with smaller down payments

- Individuals using certain loan programs

- Homebuyers seeking lower upfront costs

- Borrowers who do not meet specific lender equity requirements

What Affects Mortgage Insurance Costs?

| Factor | Potential Impact |

|---|---|

| Down Payment Amount | Smaller down payments may increase costs |

| Loan Amount | Larger loans may result in higher premiums |

| Credit Profile | Lender risk assessments may affect pricing |

| Loan Type | Requirements vary by mortgage program |

| Property Type | Certain properties may influence risk calculations |

Benefits of Mortgage Insurance

Increased Access to Homeownership

Expanded Financing Options

Lenders may offer additional loan opportunities because insurance helps reduce lending risk.

Reduced Upfront Cash Requirements

Borrowers may be able to purchase a home without accumulating a very large down payment.

Risks and Limitations

Although mortgage insurance can help borrowers access financing, it also increases the overall cost of borrowing. Premiums may be required monthly, upfront, or through another payment structure, depending on the loan arrangement.

Coverage terms, cancellation rules, and premium requirements vary by loan type and lender.

Mortgage Insurance vs Homeowners Insurance

| Feature | Mortgage Insurance | Homeowners Insurance |

|---|---|---|

| Primary Beneficiary | Lender | Property Owner |

| Protects Against Property Damage | No | Yes |

| Related to Loan Approval | Often Yes | Generally Required by Lenders |

| Focus | Loan Risk | Property Protection |

Common Mistakes Borrowers Make

- Ignoring total loan costs

- Failing to understand cancellation requirements

- Not comparing multiple loan options

- Overlooking premium structures

- Assuming all lenders have identical requirements

How to Evaluate Mortgage Insurance Requirements

Review Loan Terms Carefully

Examine all insurance-related costs included in the loan documentation.

Compare Financing Options

Different lenders and loan programs may have different insurance requirements.

Consider Long-Term Costs

Evaluate how insurance expenses affect the total cost of homeownership over time.

Things to Consider Before Obtaining a Mortgage

- Down payment amount

- Monthly budget

- Total loan costs

- Loan term length

- Property type

- Interest rates

- Long-term financial goals

This information is for educational purposes only and should not be considered financial advice.

Frequently Asked Questions

What is a mortgage?

Insurance is coverage that helps protect lenders against certain losses if a borrower defaults on a home loan.

Can a mortgage be removed?

Removal rules vary based on loan type, lender policies, and applicable regulations.