Earthquake Insurance Saves Homes is a specialized type of property coverage designed to help protect homeowners, renters, landlords, and businesses from financial losses caused by earthquakes. Standard homeowners’ insurance policies often do not cover earthquake-related damage, making separate coverage an important consideration in many regions.

Earthquakes can cause significant structural damage, destroy personal property, disrupt business operations, and create costly repair expenses. Understanding earthquake home insurance can help property owners evaluate their risks and make informed decisions about protecting valuable assets.

This guide explains how earthquake home insurance works, what it typically covers, common exclusions, benefits, limitations, and key factors to consider before purchasing a policy.

What Is Earthquake Insurance?

Earthquake insurance is a policy that provides financial protection against covered losses resulting from earthquake-related events. Coverage may apply to residential properties, commercial buildings, personal belongings, and other insured assets, depending on policy terms.

The purpose of earthquake insurance is to help policyholders recover financially after covered seismic events cause property damage.

How Earthquake Insurance Works

A property owner purchases a policy and pays premiums to maintain coverage. If a covered earthquake causes damage to insured property, the policyholder may file a claim with the insurance provider.

The insurer reviews the claim, assesses the damage, verifies that the loss resulted from a covered earthquake event, and determines the amount payable according to policy terms.

Compensation is generally subject to coverage limits, deductibles, exclusions, and other policy conditions.

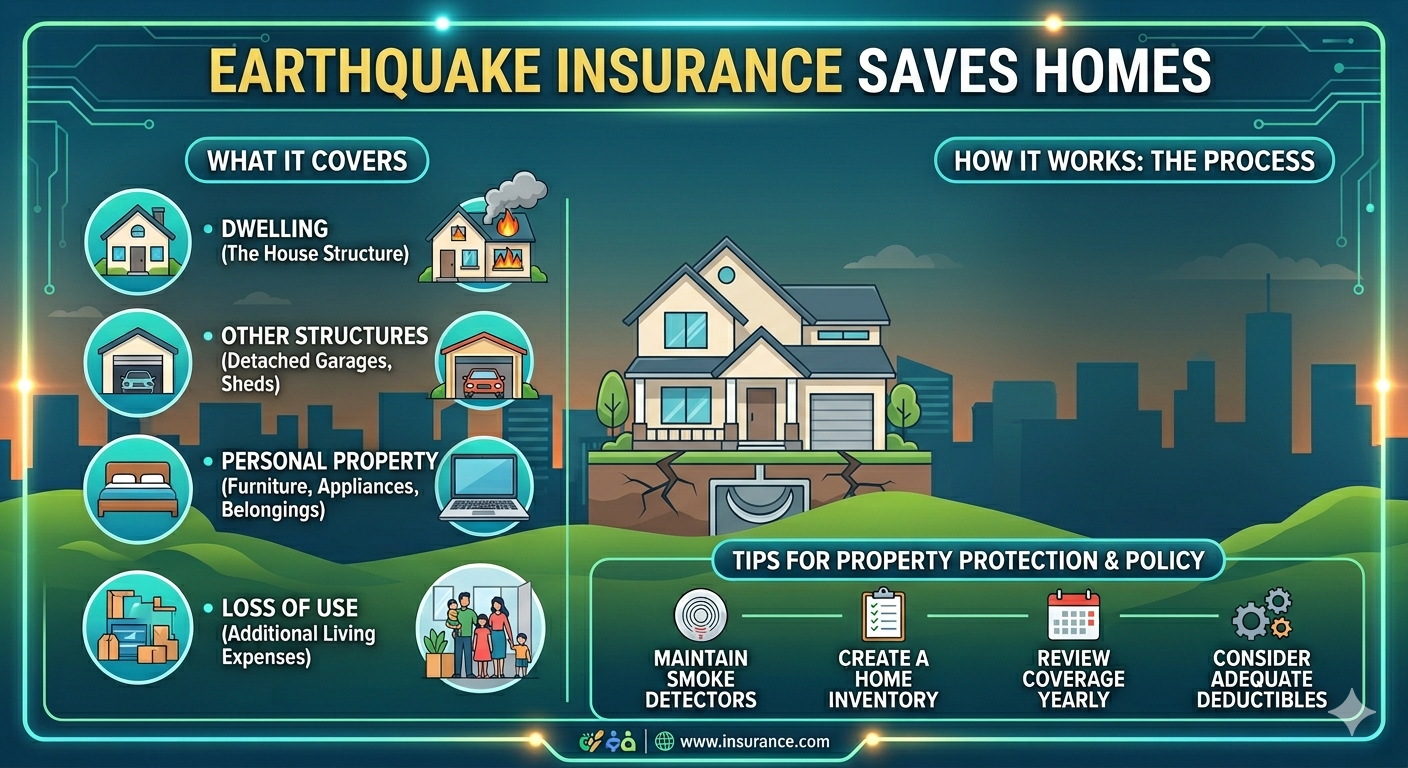

What Earthquake Insurance Typically Covers

Structural Damage

Coverage may help pay for repairs to the insured building when damage results from a covered earthquake.

- Foundation damage

- Walls and ceilings

- Roof structures

- Floors

- Built-in fixtures

- Electrical systems

- Plumbing systems

Personal Property Coverage

Some policies may help cover personal belongings damaged by earthquake-related events.

- Furniture

- Electronics

- Appliances

- Clothing

- Household items

- Personal possessions

Additional Living Expenses

Certain policies may provide coverage for temporary living expenses if a covered earthquake makes the home uninhabitable.

What Earthquake Insurance May Not Cover

Policies often contain exclusions and limitations. Common examples may include:

- Flood damage resulting from earthquakes

- Normal wear and tear

- Pre-existing structural issues

- Landscaping damage

- Vehicle damage

- Certain detached structures, unless specifically insured

Property owners should carefully review policy wording to understand coverage limitations.

Who Should Consider Earthquake Insurance?

- Homeowners in seismic regions

- Condominium owners

- Landlords

- Commercial property owners

- Business operators

- Owners of high-value properties

- Property owners seeking broader disaster protection

Even areas with moderate seismic activity may experience earthquake-related risks.

Benefits of Earthquake Insurance

Protection Against Major Property Damage

Earthquakes can cause extensive structural damage that may be expensive to repair without insurance coverage.

Financial Risk Management

Coverage can help reduce the financial impact of covered earthquake-related losses.

Protection for Personal Belongings

Some policies may provide compensation for covered personal property damaged during a seismic event.

Support During Recovery

Insurance may assist property owners as they repair or rebuild after a covered earthquake.

Coverage Beyond Standard Home Insurance

Because standard homeowners’ policies often exclude earthquake damage, separate protection may help fill an important coverage gap.

Factors Affecting Earthquake Insurance Costs

| Factor | Potential Impact |

|---|---|

| Location | Seismic risk levels affect premiums |

| Property Value | Higher values generally require more coverage |

| Building Age | Older structures may increase risk assessments |

| Construction Type | Building materials influence earthquake resistance |

| Coverage Limits | Higher limits may increase premiums |

| Deductibles | Higher deductibles may reduce premium costs |

Earthquake Insurance for Homeowners

Homeowners may use earthquake insurance to help protect both the structure of their homes and personal belongings against covered seismic losses.

Coverage requirements vary depending on location, property characteristics, and personal risk tolerance.

Earthquake Insurance for Businesses

Commercial property owners may purchase earthquake coverage to help protect buildings, equipment, inventory, machinery, and other business assets.

Business-related coverage options vary according to policy type and insurer.

Risks and Limitations of Earthquake Insurance

Although earthquake home insurance can provide valuable protection, coverage is subject to deductibles, policy limits, exclusions, and claim requirements.

Some earthquake policies have percentage-based deductibles that may be higher than those found in standard property insurance policies.

Property owners should review policy details carefully before purchasing coverage.

Common Mistakes Property Owners Make

- Assuming homeowners’ insurance covers earthquakes

- Underestimating seismic risks

- Choosing insufficient coverage limits

- Ignoring policy exclusions

- Not reviewing deductible amounts

- Failing to update coverage after renovations

- Skipping periodic policy reviews

A proactive approach can help reduce potential coverage gaps.

How to Evaluate Coverage Needs

Assess Property Value

Understanding rebuilding costs and asset values can help determine appropriate coverage limits.

Review Local Seismic Risks

Regional earthquake activity may influence insurance needs and policy selection.

Consider Deductibles

Deductible amounts can significantly affect both premium costs and claim payments.

Compare Policy Features

Coverage options, exclusions, endorsements, and limits vary among insurers.

Things to Consider Before Purchasing Coverage

- Property location

- Seismic activity levels

- Coverage limits

- Deductible structure

- Building construction type

- Policy exclusions

- Personal property protection needs

- Long-term risk management goals

This information is for educational purposes only and should not be considered financial advice.

Frequently Asked Questions

What is earthquake insurance?

Earthquake home insurance is a policy designed to help cover certain losses caused by covered earthquake events.

What does earthquake insurance cover?

Coverage may include structural damage, personal property losses, and certain additional living expenses, depending on the policy.

Who should consider earthquake insurance?

Homeowners, landlords, businesses, and property owners in seismic regions may benefit from evaluating earthquake-related risks.

Are aftershocks covered?

Coverage for aftershocks depends on policy wording and insurer guidelines.

What affects earthquake insurance costs?

Factors include location, property value, building age, construction type, coverage limits, and deductibles.

Can businesses purchase earthquake insurance?

Yes. Many businesses obtain earthquake coverage to help protect commercial buildings and business assets.