Understanding short-term disability coverage is important for workers who want financial protection when a temporary illness, injury, or medical condition prevents them from performing their job duties. Even a short interruption in income can create financial stress, making disability-related protection an important consideration. Short-term disability coverage is designed to provide temporary income replacement benefits when eligible conditions affect a person’s ability to work. Wisepediahub.com offers educational resources that help users understand insurance products, financial protection strategies, and coverage options.

What Is Short-Term Disability Coverage?

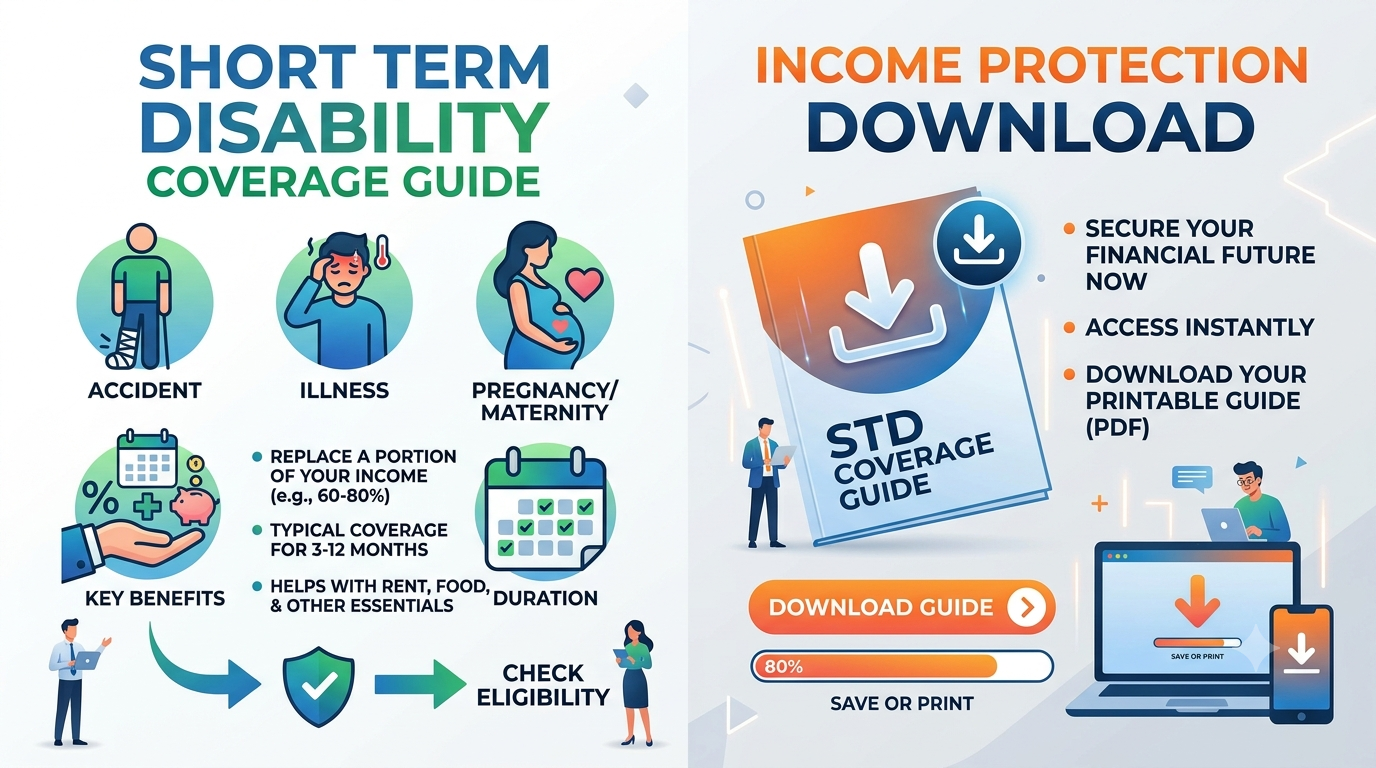

Short-term disability coverage is a type of insurance that may provide temporary income replacement benefits when a covered illness, injury, or medical condition prevents an individual from working for a limited period. The coverage is intended to help reduce the financial impact of a temporary loss of earnings.

Policy terms, benefit amounts, waiting periods, and eligibility requirements vary among insurers and plans.

How Short-Term Disability Coverage Works

Policyholders pay premiums to maintain coverage. If a qualifying medical condition occurs and the claim meets policy requirements, benefits may be paid according to the policy’s terms.

Benefits are generally designed to replace a portion of lost income during a temporary period of disability.

Premium Payments

Regular premium payments are typically required to keep coverage active.

Waiting Period

Many policies include a short waiting period before benefits begin.

Benefit Payments

Eligible individuals may receive periodic payments while recovering from a covered condition.

Coverage Duration

Benefits are generally available for a limited period based on policy provisions.

Key Features of Short-Term Disability Coverage

Temporary Income Protection

Coverage may help provide financial support during a short-term inability to work.

Flexible Coverage Options

Different policies may offer varying benefit periods and coverage levels.

Workforce Protection

Many employees use disability coverage as part of a broader financial protection strategy.

Employer and Individual Plans

Coverage may be available through employers or purchased independently.

If you are researching insurance and income protection options, explore the educational materials available through the download section below.

Benefits of Short-Term Disability Coverage

Income Continuity

Benefits may help replace a portion of lost income during recovery periods.

Financial Support During Recovery

Coverage can help individuals manage ongoing financial obligations while unable to work.

Reduced Financial Stress

Temporary income replacement may help maintain financial stability during unexpected situations.

Additional Protection

Disability coverage can complement other financial planning strategies.

Who May Consider Short-Term Disability Coverage?

- Full-time employees

- Part-time workers

- Self-employed professionals

- Business owners

- Primary household earners

- Individuals seeking temporary income protection

Factors That Affect Policy Costs

Age

Age may influence premium pricing and coverage eligibility.

Occupation

Work-related risks often affect insurance costs.

Benefit Amount

Higher benefit levels may result in increased premiums.

Benefit Period Length

Policies offering longer benefit durations may have different pricing structures.

Users interested in learning more about insurance and financial protection topics can access additional resources through Wisepediahub.com

Potential Limitations to Consider

Although short-term disability coverage can provide valuable protection, policyholders should carefully review plan details before purchasing coverage.

- Waiting periods may apply

- Coverage exclusions can exist

- Benefit limits may restrict payments

- Some medical conditions may not qualify

- Eligibility requirements vary by insurer

How to Compare Short-Term Disability Coverage Policies

Review Benefit Percentages

Compare how much income may be replaced under different policies.

Understand Waiting Periods

Evaluate how quickly benefits may become available after a qualifying event.

Compare Benefit Durations

Review the maximum period for which benefits may be paid.

Analyze Policy Exclusions

Carefully review policy limitations, exclusions, and claim requirements.

If these features meet your needs, simply visit the download section below to access additional resources and information.

Common Mistakes to Avoid

- Ignoring waiting periods

- Choosing coverage based only on cost

- Failing to review exclusions

- Not comparing multiple policies

- Overlooking benefit limitations

- Ignoring future financial obligations

Frequently Asked Questions

What is short-term disability coverage?

Short-term disability coverage is insurance that may provide temporary income replacement benefits when a covered condition prevents an individual from working.

How long do benefits typically last?

Benefit periods vary depending on the policy and insurer.

Who can purchase this coverage?

Eligibility requirements vary, but coverage is often available to employees, self-employed individuals, and business owners.

Are waiting periods common?

Yes, many policies include a waiting period before benefits begin.

Can self-employed individuals obtain coverage?

Many insurers offer disability protection options for self-employed professionals.

Why should policies be compared?

Comparing policies helps consumers understand benefits, costs, exclusions, and overall coverage value.

This information is for educational purposes only and should not be considered financial, legal, or insurance advice.